The recent “Trump Tariffs” are a powerful reminder that markets can become volatile during times of uncertainty. Around the world, markets have been fluctuating widely as investors struggle to understand an escalating trade war, particularly between the US and China. As investors, what should we do…

April can be a time of financial opportunity and challenges. The new financial year begins on 6 April, bringing a fresh set of allowances – potentially helping you save on tax. However, the new tax year can also bring different tax thresholds and deductions, potentially increasing outgoings or take-home pay…

Are you thinking about picking up some work after retiring? Perhaps you are even considering a full return to the workforce. In 2025, many people are considering “unretirement” in some form – some out of necessity, others out of choice. In this guide, our financial planners explain the nature…

Divorce can be one of life’s most stressful and destabilising events. Psychologically, the death of a spouse is the only experience regarded as more difficult. Given the upheaval involved, it is not surprising that financial mistakes are often made – sometimes haunting people for years…

Are you looking to put more hard-earned money back in your pocket? With a robust financial plan, taxpayers can mitigate needless taxes on their income and assets. This is especially important in 2024-25 when housing and other living costs continue to rise. Below, our Burnley financial planners offer some ideas…

Did you know that around 1.2 million people are “mostly reliant” on the State Pension? 28% of over 55-year-olds are completely dependent on it, with no other pension savings. This raises the question: can you get by purely on the State Pension in retirement? Below, our Burnley financial advisers explain…

Investing can feel overwhelming even for experienced investors. The jargon and assets can be very confusing. What are equities, fixed-income investments, and commodities, for instance? What do they “do”, and how can they be integrated into an investment strategy? In this guide, our Burnley financial advisers explain…

How can you unlock the value tied up in your property? You may be looking for ways to fund retirement. Or, you may want to fund some home improvements. Below, our Burnley financial advisers discuss two options: downsizing and equity release. This guide outlines the main pros and cons of each approach…

The Prime Minister has warned that the upcoming Autumn Statement (due on 30 October) will be “painful”. Before this, the Chancellor – Rachel Reeves – confirmed that tax rises will be necessary in the budget. Naturally, investor and business confidence is down to their lowest levels since December 2022…

Pensions are highly effective for retirement planning. They can offer generous tax breaks (such as tax relief on contributions), significantly boosting a nest egg’s growth over time. However, pensions can also be confusing. Not only do different types of pensions exist, but the rules and processes can vary…

Interest rates have been steadily falling across the Western world in 2024. The European Central Bank (ECB) cut rates twice in three months, now at 3.65% for main refinancing operations. In the US, the Federal Reserve made an aggressive half-point cut in September. The Bank of England (BoE) also cut…

Almost a year has passed since the atrocities in Israel on 7 October 2023. Now, the Middle East is escalating in conflict. No longer restricted to Gaza, hostilities are taking place across the region, including Yemen and Lebanon. With the world bracing for a potential outright war between Israel and Iran…

The election is finally over. Labour won convincingly on 4 July with a large majority, unseating the incumbents after 14 years of power. Pundits are now exploring how the new government might change key policy areas in the coming weeks and months. In particular, are any taxes set to change…

What is happening in the UK economy? Are things “getting better” in the summer of 2024, or worse? How might the landscape change, and what are the implications for your financial plan? Below, our financial planners explore some of these questions in more detail. We hope these insights are helpful…

Being single – whether by choice or involuntarily – brings many unique opportunities and challenges for financial planning. Perhaps you imagine yourself living independently in retirement. Or, maybe you find yourself suddenly single due to divorce or bereavement. Regardless of the circumstances…

The UK’s median employee turnover (“churn”) rate is 15%, according to the CIPD (Chartered Institute of Personnel and Development). Alarmingly for employers, replacing a mid-level employee can cost over £30,000 when costs such as temporary worker hire, lost productivity and training…

The Spring Budget of 2024 brought a range of key changes which bear upon UK households (not least the “headline” measure to cut National Insurance). Below, our Padiham financial advisers elaborate on our recent Budget Special newsletter to explain, in more detail, how readers’ financial plans may be impacted…

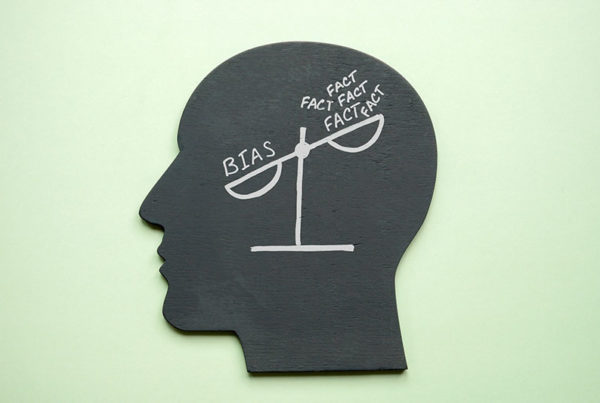

Many great stories and sagas build on the theme of an “inner battle” within the self. Great investors also experience this reality. Various “biases” try to pull them towards irrational decisions with their investments. Yet, how can you conquer the irrational assumptions, beliefs and temptations which may lead you to act…

The new tax year (2024-25) started on 6 April 2024. This brings a fresh opportunity to get the most out of your allowances and put more hard-earned money back into your pocket. Below, we discuss some key changes to know about in the new tax year, offering ideas about how to maximise your financial…

Many people dream of retiring early. The thought of enjoying more time for travel, family, and passion projects is certainly appealing. However, “early retirement” has undergone a significant generational change. In previous decades, men often retired earlier than women. There were “send off”…